We’ve written in the past about the precautions and procedures that Cumberland Title uses to keep your information safe while it’s in our hands. But there are also some pretty simple but important steps that everyone can take to keep their personal workstations safe and secure from fraud.

These days, simply locking your office door isn’t enough to stay safe in today’s fast-paced business world. It’s important to remember that cyber thieves aren’t the only threats lurking, and that keeping our workstations themselves from falling prey to threats and risks is also important.

Here are a few steps you can take to keep your workspace protected:

- Don’t leave your office without first clearing off your desk. It’s important to make sure that confidential data is locked away and not left out in the open. Locking the door to the office is also highly recommended

- Recycle bin vs. Shred bin. I’m all for recycling, but make sure that the things that are going in the blue bin do not have sensitive information on them. If so, they go in the shred bin (which should also remain locked)

- Passwords: Yes, it can be a real pain to have and have to remember multiple passwords for different systems, and it may seem convenient to use the same one for all systems, or choose one that’s simple to remember—or even share it with co-workers. Lest we learn nothing from the 2016 Verizon Data Breach Report which confirmed that 63% of confirmed data breaches were a result of weak, default, or stolen passwords.

- Mobile devices. Where to begin with this one… Imagine losing your work issued cell phone, or having it stolen. Treat this device like you should your work computer, and lock it up! That’s right, password protect that sucker, too. And remember to back up that data in the event it is lost or stolen. A leading study showed that in the event of thefts involving mobile devices, 25% occur in cars and transportation, 23% in the office, and 15% in airports and hotels.

- Working in public on a laptop. Thieves are opportunists who will seize any opportunity, especially when you make it so tempting and easy for them. They are not above looking over your shoulder at your screen or stealing hardcopy papers you may have lying next to you, should you step away for only a second to grab an extra sugar for your coffee. Don’t make it any easier for them.

For those of us who have been in a real estate closing – regardless of what side you’re on – you can appreciate that there are a LOT of checks and balances happening during that transaction, let alone an enormous amount of paperwork.

Aside from procuring the necessary documents, ordering payoffs, checking taxes and titles, and putting together all of the necessary documents, it is the title company’s responsibility to ensure that funding has been received. It is extremely important to note that the transaction cannot be completed until that check or wire is received. Even if all the paperwork has been signed and that’s all you’re waiting around for. No money = no completed transaction.

Likewise, if would be irresponsible for the title company to hand out any checks before the transaction has been officially funded. Any title company or settlement agency that plays by the rules knows that this is actually a violation of the Bar Rules governing attorneys, Maine’s statutes, and quite possibly a violation of most lender’s closing instructions. To do this would put many parties involved in the transaction in a very precarious – and culpable – position.

From the perspective of a title company, trust accounts are highly regulated as they contain money that does not belong to them. The money contained in them belongs to other people who have transacted business through their company. They should never be using funds from one customer to fund a transaction for another customer. And by handing out checks before funds are received, that is essentially the exact scenario that is happening.

One very important point to note here also, is that Maine is what’s called a “wet funding state”. In short, that means that closings are not even supposed to happen without funding that is available to the parties. Many other states have an escrow system when real estate is transferred, where it’s a matter of course that checks are not given at the table (dry funding states), and the closing is essentially done in escrow. But checks are not handed out in this case either.

From a customer service perspective, Cumberland Title aims for all of our closings to be smooth and error-free. Unfortunately, there are times when a wire is taking longer than anticipated to reach us before the conclusion of signing the closing documents, and rather than just saying, “Oh, I’m sure it’s on the way, let’s just call it good and get you all on your way”, we have to cross all the T’s and dot all the I’s in accordance to the law as well as the procedures we have in place that are designed to protect all parties involved in the transaction. This all amounts to both legal and ethical concerns, both State law as well as attorney Rules of Ethics.

As always, we are always here to answer your questions and shed light on the parts of the process that may seem unclear or confusing. We pride ourselves on our reputation for clear, concise, transparent transactions and communication. Please do not hesitate to reach out to us at 207.899.4900, or matthew@cumberlandtitle.com.

Cumberland Title is proud to employ some of the best and hardest working talent in the title insurance business. We’d like to take this opportunity to introduce you to the newest member of the Cumberland Title Team!

Name: Melissa M. Donahue

Title: Title Attorney

How long have you worked at Cumberland Title, and which location do you work out of?

I joined Cumberland Title in July, 2018. I work in our Portland office at 178 Middle Street.

What is your role at Cumberland Title?

I am a title attorney for Cumberland Title. I do all manner of legal document review and preparation for all of our locations. I also assist with preparing title commitments, conduct closings, and answering any legal questions our lenders, buyers and sellers may have.

What is the best part of your job?

The best part of my job is the people I work for. Matthew and Randee McDonald are extremely kind and thoughtful leaders. I am proud that they chose me to work for them.

What is the hardest part of your job?

For me, the most difficult part of the job is delivering bad news to our clients when it comes to title issues. I work hard to find and create solutions so each closing can move forward smoothly and in a timely manner. Some title issues just can’t be resolved without some form of legal action and sometimes we just can’t get the fix we need in time.

What do you wish people knew about title insurance / title companies in general?

I wish more people knew that it is not our intention to be an obstacle between them and buying and/or selling their homes. We strive to be as thorough as possible to avoid future issues for our lender clients, buyers and sellers. While some may view our unwillingness to cut corners as a hindrance, those who work with us can rest assured that we have done everything in our power to minimize the risk of future title issues.

Easements: What You Need to Know

The word “easement” is defined as, “a right to cross or otherwise use someone else’s land for a specified purpose.” In its simplest terms, a property easement allows for a third party to use a portion of someone else’s property for a specific use. Most commonly we see this as a “right of way” issue or to allow service maintenance – such as utility companies – to access a certain piece of land.

Easements can also exist to address a number of issues. Reasons for easements can differ depending on the situation, such as an easement of necessity, a private easement, or a utility easement

One example would be if the only way to access Property B from a main road is to go through an alley or driveway that is located on a neighboring Property A, then property A would most likely be burdened with an easement that benefits Property B.

Another example would be if electric lines are located above Property A and Property B, then both properties would most likely be burdened with easements that benefit the electric company so that they can access either property in the event they need to repair or maintain those electric lines.

But what does this all actually mean to the homeowner who has the easement attached to their property?

If you have an easement attached to your land, you are not permitted to build any structure on or over the easement land, or to use it in any way that interferes with the rights of the party benefitting from the easement. Failure to comply could actually result in the new structure built on the easement to be destroyed, or the homeowner could even be sued.

When you work with Cumberland Title, you can be confident that we conduct thorough title searches and will disclose if we find any easements – as well as liens or encroachments – and we will share that information on the title report prior to closing. And as always, we are here to answer any questions you may have about the title search process, or any other aspect of your real estate transaction and closing.

Title Insurance for Manufactured & Mobile Homes – A Quick Overview

The way that mobile homes & manufactured homes are handled is a little bit different than a standard real estate closing.

Anything related to real property (real estate), must be recorded in the Registry of Deeds in order for it to be valid on a title or subject to a lien. However, some mobile homes could also be considered motor vehicles, or personal property. In this case, instead of being recorded at the Registry of Deeds or discovered during the title search, a lien on a motor vehicle would actually be noted on the vehicle’s certificate of title. Therefore if the title company only searched the Registry of Deeds, they could miss something huge if they don’t also check the Secretary of State’s records, where motor vehicle and personal property is recorded.

Also important to note is in the case of manufactured “pre fab” homes, the individual pre fab pieces that are delivered to the land are considered personal property until they are erected into a finished dwelling and attached to the land.

Likewise, a mobile home becomes a home and no longer a vehicle once the wheels, axle and tongue have been removed, the home has permanently been affixed to the land on a permanent foundation, and the title has been cancelled with all other state agencies (ie: Secretary of State’s office) that handle mobile homes in the state of origin and the state it’s been affixed to land in.

If you have questions about title insurance and how that applies to a mobile home, give us a call, we’re happy to help, 207-899-4900.

You’ve been assigned your date, time and location for your property transaction closing, but you’re not in the clear yet! There are still some things that can compromise the closing and prevent it from happening. Heed this warning and make sure you or your clients do not fall victim to these issues:

- Power of Attorney Issues

- Cumberland Title can and will – and prefers – to draft this document in our office so we know for sure it will be correct and acceptable for use at the closing, and no issues will arise as a result.

- There is specific information that must be contained in a Power of Attorney to be valid for a real estate closing. Some people attempt to draft one themselves and have it notarized and bring it with them to the closing. Unfortunately, if the document is deemed invalid for use in this transaction, the closing cannot happen.

- Out of State Parties (2.5% Withholding)

- If you are selling a home in Maine, for example, and Maine is not considered your permanent residence state, you will be subject to the 2.5% Out of State Withholding tax. Make sure this is addressed before the closing, or you won’t be closing that day due to additional paperwork needing to be submitted.

- In the case of those that consider themselves “snow birds” or split their time between two homes in different states, the state where they reside a total of 6 months + 1 day or more, is considered their legal residence.

- The state in which you are domiciled is considered your permanent legal residence. If you move out of Maine temporarily, without establishing domicile in the other state (or country), you continue to be domiciled in Maine. This is the case even if you sell your home in Maine.

- Last Minute Changes

- We cannot stress this one enough – DO NOT pay anything or change anything in the days leading up to the closing. This includes – but is not limited to – taxes, homeowner’s insurance, home equity lines, in-store credit cards. All of these things affect the outcome of the already approved closing details/figures, which will then be incorrect and new documents need to be issued by lender and title company.

- Funding Issues

- Also, please do not bring cash to a closing. A bank check just better protects both you and the title company – who most definitely doesn’t want to have to walk to the bank with that in hand to deposit it. Too many risks here.

- If your funds are being wired to the title company, make sure that you allow time for that wire to come through to the title company. Wires do not necessarily happen “automatically”, and can take up to a few hours to arrive into the account. If there’s no money, there’s no closing.

- If you were instructed to bring a check to closing, make sure that you do. If you were told that it had to be a bank check and not a personal check, make sure that it is.

- Side Deals Discussed At The Closing Table

- So if you want to ask the seller if you can buy his ride on mower, too, make sure you do that before or after the closing.

- Under no circumstances are any side deals or transactions to be discussed at the closing table during the real estate transaction. In fact, if this does occur, TRID rules require that the title company stop the closing immediately and not allow it to continue.

- Improper ID

- You are required to provide proof of identity at your closing. Both the lender and the title company require this. When you check in to the title company, chances are they are going to ask you for this right up front. You should be prepared to hand them a current, valid ID with photo. Think driver’s license, state ID, or passport. These should be valid and not expired. No ID = no closing.

A real estate closing should be a happy occasion. Please do your best to avoid these scenarios that will turn this happy occasion into a frustrating one. And a good rule of thumb, if you are unsure about ANYTHING leading up to the closing date, call your lender or title company for guidance.

Q: Does it make sense to get title insurance on a condo that was recently built if you intend to pay for it in cash?

A: Absolutely. Title Insurance will defend against all potential claims going forward for as long as you own the property. It’s really a small, one-time price to pay to avoid all future headaches. The cost of coverage is far less than any future litigation would be in the event that there is a title claim/issue. This will also be handy in regards to the future sale of the property.

Q: Why do I have to purchase title insurance every time I refinance my house?

A: Lender’s title insurance needs to be purchased each time you refinance your home, as this is a safety measure that lender’s (banks, mortgage companies) require to protect themselves. When you refinance, the lender needs to be sure that there are no liens that have popped up on the property since the last policy was purchased, or other such issue. Also, the policy needs to reflect the current value of the home, in the even that differs from the last policy due to home renovations or improvements, for example.

Q: What kind of problems can a title search reveal?

A: A title search can reveal a number of title defects and liens, as well as other encumbrances and restrictions. These can include unpaid taxes, unsatisfied mortgages, judgements against the seller, and restrictions limiting use of the land.

Q: How does title insurance protect my investment in the event that a claim should arise?

A: If a claim is made against your property, according to the terms of your title insurance policy, you will be assured of a legal defense, including payment of all court costs and related fees. Also, if the claim does prove valid, you will be reimbursed for your actual loss up to the face amount of the policy.

Q: The owner of the property I’m purchasing only lived there for 6 months. If he had a title search done just 6 months ago, why do I need another one?

A: Because the owner could, in a very short time, do many things to encumber the title. For example, he could grant easements or construction improvements that encroach on the adjacent property. HE could have used the property as collateral for a loan, or received a judgement or lien that can attach to the real estate. It is always necessary to conduct an up to date title search to uncover any such problems.

Q: How long does my title insurance coverage last?

A: For as long as you or your heirs retain an interest in the property.

Q: If the builder of my home already has title insurance on the property, why do I need it again when I purchase the land from him?

A: A title policy insuring the builder does not protect you. Not to mention, many things could have happened to the land since the builder’s policy was issued. There could be an increase in value, which calls for additional coverage. Liens, judgements, or unpaid taxes – from either the builders or prior owners – may be disclosed after you purchase the property.

Recently, a real estate agent asked me if she should be marketing her listing by including the fact that the seller is willing to accept Bitcoin. If you don’t know what Bitcoin is, the simplest definition I can come up with is that Bitcoin is a digital currency and it, along with other cryptocurrencies, are going to change…everything. Here was my answer to her:

Good News and Bad News as they say. First of all, I’m the right guy to ask because I’m a cryptocurrency fan. I’ve been buying, selling and well just holding about 16 different cryptocurrencies for about a year now.

While I think Bitcoin and other cryptocurrencies are indeed THE future of money and transactions, we just aren’t there yet. Bitcoin and others fall into a legal gray area when it comes to being recognized as payments. So while I have read about some real estate transactions that were accomplished around the country using Bitcoin, most likely the Bitcoin was converted to dollars “at the table” and then the transaction happened.

The other thing about Bitcoin is that it is wicked volatile. $9,424 at this time. By the time you read this email it could have swung by $500 up or down easily. So let’s say you were selling a house for 500k. That would be 53.03 bitcoin. Like I said, the price of Bitcoin could rise or fall quickly. If the price of Bitcoin were to go down by $800 in one hour (about the time for a closing to happen) then your seller effectively sold for 457k. Conversely, the buyer could overpay by tens of thousands of dollars if the price skyrocketed. Your commission of 3% could rise or fall by 5, 10 maybe even 15% by the time you get back to your car after the transaction! Wow.

So while it is very interesting to sell a property for Bitcoin I would not recommend it at this time. The final nail in the coffin is that the title insurance companies cannot insure transactions with Bitcoin. That means that you would not be able to get a loan for the property restricting the pool of buyers to cash buyers, or well “Bitcoin buyers.”

There are many experts who say cryptocurrencies are a fad and are destined to value at zero. But those are the people who are most threatened by cryptocurrencies. I can find experts who will tell you with an absolute straight face that a Bitcoin will be worth one million dollars by 2020. Let’s hope they are right! The truth lies somewhere in the middle but I KNOW this….. Our grandkids will be using cryptocurrencies every day for all kinds of purchases, including real estate.

Bitcoin is the most well known cryptocurrency but there are hundreds of different cryptos being developed for all kinds of projects. Burstcoin is an environmentally friendly cryptocurrency alternative to Bitcoin. (Bitcoin uses a LOT of power) Ethereum features “smart contracts” which could aid in real estate transactions. There are other coins being developed specifically for real estate transactions.

So while we may not be using Bitcoin, Burstcoin or Ethereum right now, our kids sure will.

Have a burning question about title insurance or the real estate closing process? We have the answers! We love to education and inform consumers – and industry professionals – about the intricacies of the business. Send your queries to matthew@cumberlandtitle.com.

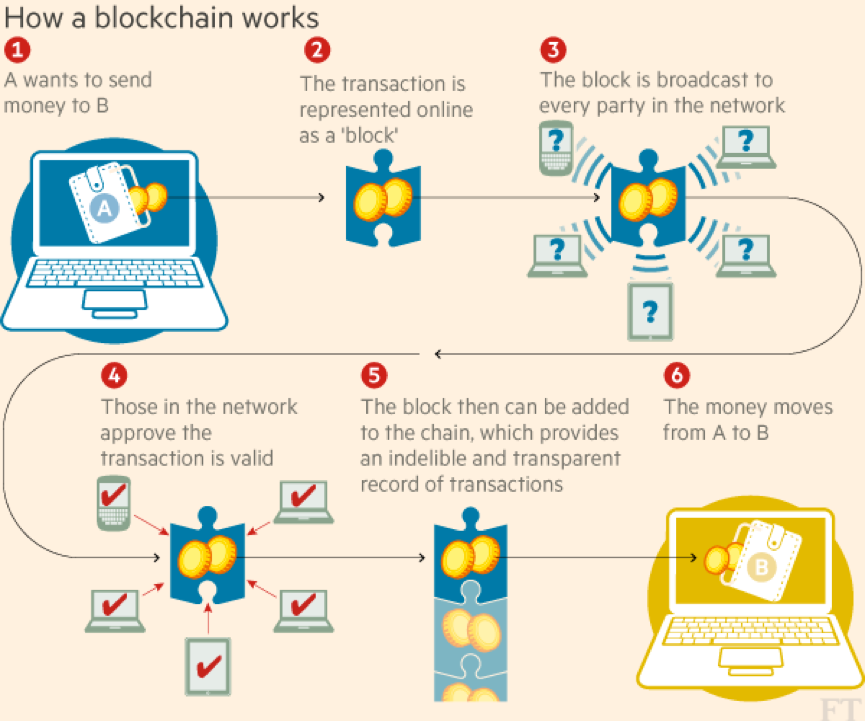

In the simplest terms, blockchain is the ability to remotely share databases and processes, making them more centralized and accessible. For the real estate industry specifically, this could transform the industry by making it more modern and efficient.

One such way is accessing the MLS Property Data system. Every real estate transaction goes through the MLS service which tracks agents, clients, contracts, listing agreements, appraisals, etc. Unfortunately the information on the MLS is often decentralized and restricted, and it’s often out of date.

Blockchain technology can be used to overcome these barriers. By providing a way to securely share data, the blockchain makes a shared, nationwide database possible, one that offers real-time access to property information straight from the source and enables a more holistic view. It also opens up more opportunities for collaboration among players in the real estate industry.

The blockchain can also provide a central title database for the entire country to securely store and instantly access historical title records, allowing for the streamlining of title transfer in a property sale.

Another very important area that the blockchain will effect is the efficiency and security of transactions. Each user has a unique identity on the blockchain via cryptography, which means consumer financial information can be shared securely with other parties during transactions. One person can send funds to another person that won’t release until the transaction is formally completed. This adds a layer of security that speeds up the transaction management process regardless of whether the buyer and seller are in the same place.

Blockchain technology streamlines the real estate process by enabling people to securely and efficiently share data and money. It makes information more accessible, cuts out the middlemen, and reduces the risks of fraud and theft. Currently only a couple states are experimenting with this technology with a few more slated to give it a try. Could Maine be far behind? We’ll have to wait and see. (see the below infographic for a visual explanation of how blockchain works)